Borrowers, beware: Tribal-affiliated loans sound good, but can cost a lot

The Minnesota attorney general’s workplace claims consumers will get by themselves in murky appropriate waters.

This short article had been monitored by MinnPost journalist Sharon Schmickle, manufactured in partnership with pupils in the University of Minnesota class of Journalism and Mass Communication, and it is one out of a number of periodic articles funded by way of a grant through the Northwest region Foundation.

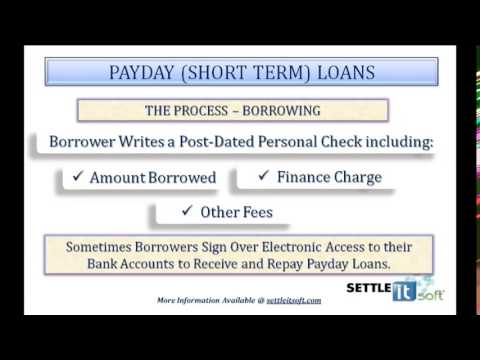

Catch a sports broadcast in Minnesota, and you’re likely to see fast-cash commercials with a appropriate twist: you may get hundreds – even, thousands – of dollars in your bank checking account the next day. No security required. And don’t worry about state-imposed loan limitations because this deal would result from a native business that is american-owned.

Simple cash? Not always. Borrowers who bite on these advertisements are able to find on their own in murky appropriate waters where regulators are powerless to greatly help them settle disputes and courts can’t agree with the reach of tribal sovereignty.

Huge number of borrowers have  reported to governing bodies nationwide about difficulties with tribal-affiliated loans. They’ve alleged that their bank reports had been tapped for costs up to 3 times the loan that is original, their wages were improperly garnished by remote tribal courts and their objections had been met by threats of arrests and legal actions.

reported to governing bodies nationwide about difficulties with tribal-affiliated loans. They’ve alleged that their bank reports had been tapped for costs up to 3 times the loan that is original, their wages were improperly garnished by remote tribal courts and their objections had been met by threats of arrests and legal actions.

In Minnesota, Attorney General Lori Swanson has introduced some such complaints into the Consumer that is national Financial Bureau, said her spokesman Benjamin Wogsland.

Numerous tribal financing organizations are genuine, since will be the tribes’ sovereign liberties to use them by themselves terms. Certainly, one Minnesota tribe, the Mille Lacs Band of Ojibwe, has a respected string of federally chartered banks.

However in the bold realm of online financing, some non-Indian players are utilising tribal sovereign resistance as a front side – so-called “rent-a-tribe” schemes – so that you can dodge state limitations on loan quantities, rates of interest and collection strategies, federal authorities allege.

“These payday lenders are just like amoebas, they keep changing types,” Wogsland said. “The small man is getting pounded by these loans.”

Minnesota crackdown

Swanson has relocated recently to break straight straight straight down on non-Indian lenders that are online had been running illegally in Minnesota. May 31, Ramsey County District Judge Margaret Marrinan ordered Delaware-based Integrity Advance LLC to cover $7 million in damages to your state along with $705,308 in restitution to Minnesota borrowers.

The organization additionally had been barred from gathering interest and charges on loans issued to Minnesotans unless it becomes correctly certified when you look at the state. Integrity initially denied it had granted at least 1,269 payday loans in the state that it was lending to Minnesotans, but Swanson’s office compiled evidence indicating. It had charged Minnesota borrowers interest prices as much as 1,369 per cent, far more than caps occur state legislation, the judge stated.

The outcome had been the eighth court that is recent Swanson’s workplace has scored against online loan providers. Is she now establishing her places in the loan providers whom claim tribal resistance to obtain around state legislation? Wogsland stated he could neither verify nor reject any research.

Wogsland did state, though, that work is “aware” of issues with online loan providers “claiming they have been somehow resistant through the legislation due to some type of sovereignty.” The concern, he stated, arises as soon as the financing operations “are maybe maybe not really run with a tribal device however it’s perhaps only a rent-a-tribe scenario or a person user claiming that they’ve got sovereignty and that the laws and regulations don’t apply to them.”

The brand new casino

You can easily realise why lending that is online other designs of e-commerce interest tribes, particularly those on remote reservations where casino returns happen disappointing, and ultra-high jobless continues.

Think about the online loan company once the brand new casino, a new opportunity to raise the everyday lives of impoverished individuals. In reality, the appropriate thinking is just like the argument United states Indians deployed a lot more than two decades ago to launch a brand new age of casino gambling. It holds that tribal companies have actually sovereign liberties to create their very own guidelines.

Can it be the exact same, though, if the continuing business provides loans to borrowers that are maybe not on tribal land? Planning to a booking to try out slots is something. Can it be comparable for anyone to stay within an workplace on a reservation that is indian negotiate that loan via Web and/or phone by having a debtor that is in, state, Mankato or Anoka or Hibbing?

A few states have said no. Additionally the U.S. Federal Trade Commission has relocated in federal court to reign in certain tribal-affiliated loan providers.